How NYC Property Taxes are Calculated

Part 1 of an assessment of NYC property taxes

The simplified formula for Property Taxes is

(Market Value * Assessment Ratio - Exemptions) * (Tax Rate) - Abatements

… but the actual calculation is anything but simple.

Some Takeaways

The rest of the post fleshes out the details, but if you want to skip to the end

The NYC Department of Finance (DOF) is responsible for Property Valuations and Assessments

Total Valuations limit the amount of Property Taxes the City can levy for its Operating Expenses under the State Constitution. The City is VERY close to the Property Tax limit and it is unclear how much they can be raised

State law constrains how the DOF can fulfill its role, but the DOF has far more power than you might think

The DOF can, in effect, raise or lower Assessment Caps on 1-3 family homes taxes by lowering or raising their Assessment Ratio. This can ameliorate or exacerbate the tax inequity between neighborhoods that have appreciated rapidly (Park Slope) and those that haven’t (Canarsie)

The DOF is not required to, and arguably forbidden from, valuing older Co-ops as though they are rent-stabilized buildings. However, that is what they do which means the most desirable pre-war co-ops pay similar taxes per square foot as pre-1974 stabilized rentals

Valuations within a Class mostly do NOT affect the overall Property Taxes of that class since tax rates are set to hold the Class share of taxes constant. Low absolute values for Condos don’t matter in and of themselves, but their low value relative value to rental buildings shifts the tax burden onto renters.

Active litigation (TENNY v City of New York) has the potential to compel the City to change Class 1 and 2 Assessments to reduce these inequalities

A subsequent post will demonstrate how this works as applied using property level tax data, but I have to get a lot of words out of the way first. Sorry!

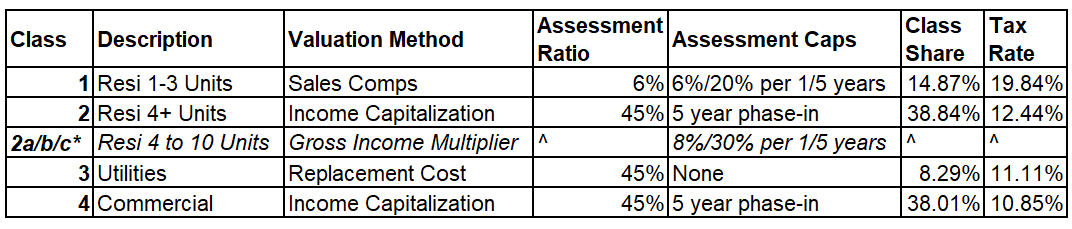

Property Classes

There’s more history here than we need, so we’ll start somewhere in the middle. For tax purposes, there are four classes of property in NYC as defined by NYS RPT Article 18. Nassau County, another Special Assessing Unit, also uses this system while the rest of the state follows a different system.

*2a, 2b and 2c are sub-classes of Class 2 with special Valuation Methods and Assessment Caps. They do not have independent Assessment Ratios, Class Shares or Tax Rates

https://www.nyc.gov/assets/omb/downloads/pdf/tax/methodology-2025-10.pdf

Every property is assigned to a Class and that forms the basis for the subsequent calculations.

Market Value

Given these classifications, the DOF estimates the Market Value for over 1 million parcels in NYC.

The valuation method they use depends on the class, shown in the table above. These methods aren’t codified in statute, but are generally accepted per State guidance and NY Court holdings.

Sales Comps - Just what it sounds like. The DOF looks at sales prices of comparable properties to estimate market value. Corresponds closely to a true market value. This is the preferred method for Class 1 and what NYC uses.

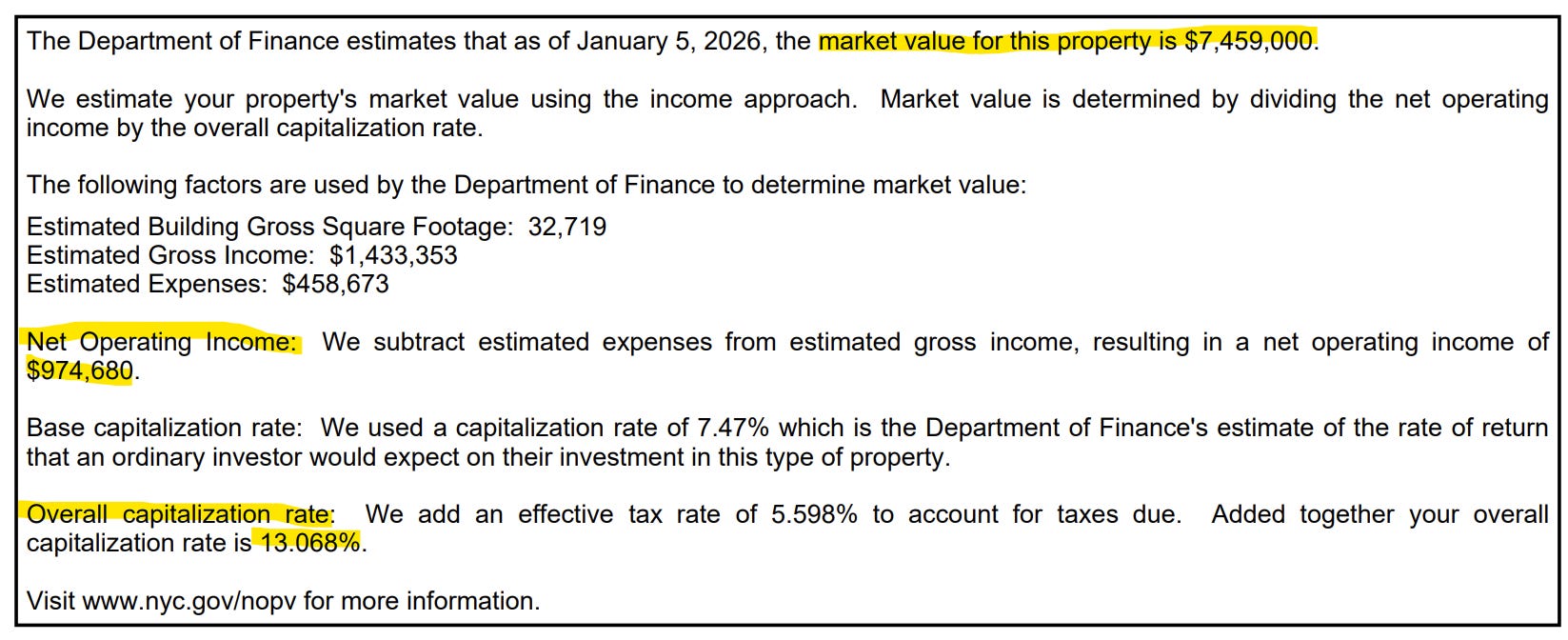

Income Capitalization - For rental buildings, DOF estimates Net Operating Income (NOI) from buildings’ annual Real Property Income and Expense (RPIE) filings and divides by a Capitalization Rate (Cap Rate).

Market Value = NOI / Cap Rate

The higher the Cap Rate, the lower the Market Value. Here’s an example

The DOF estimates NOI as $974,680 and divides that by a 13.068% Cap Rate to get a $7,459,000 Market Value.

If you are familiar with typical real estate Cap Rates, that number will sound far too high. This is because the DOF excludes tax expenses in calculating NOI and then uses an add-on to the Cap Rate to account for it

That’s not the normal way finance folks do it, but in New York we like to use our own definitions (see also: New York Supreme Courts and the NYC Administrative Code)

The Base Cap Rates shown here are a little more apples-to-apples with what real estate investors would expect

Arguably the DOF could switch to a Sales approach for rentals, but this would be somewhat unusual and subject to challenge (Merrick v Board of Assessors 1978 affirms income capitalization as the standard method for rental property but doesn’t foreclose a sales approach where reliable data exists). Practically, there is also far less sales data for rental buildings which would make this challenging.

So far so good. Where this gets strange and highly controversial is how this applies to co-ops and condos.

The DOF uses “comparable” rental building data for their valuations as they don’t typically have rental income. Why would they use rental income at all? Because NYS RPTL Section 581 says co-ops and condos have to be valued no higher than as if they were rentals.

Within these bounds, it is mostly up to the DOF to select which rentals are used for the comparison. They provide the comparables they use for each Co-op and Condo building here

It is not hard to find absurd comps. In fact most of the rental buildings used are Rent Stabilized which artificially depresses the valuation of co-ops and condos. As noted by the Court of Appeals in TENNY

The assessment methodology for these properties is undisputed: “[a]s a matter of [DOF] policy, all cooperative and condominium units constructed before 1974—a category that includes 98% of cooperative apartments in the City—are valued under the income approach by comparison to rental properties that were built before 1974” and, “[b]ecause of the City’s rent stabilization laws, this effectively means that older cooperatives and condominiums are compared to buildings whose income is suppressed by rent stabilization, even though those cooperative and condominium units do not and could not qualify for rent stabilization and are, in fact, sold (and rented) at much higher market values.

Here is a full-service Prospect Heights Coop with sales prices around $1000 / sqft. It is valued as though it were a rent stabilized building worth $156/sqft, charging $2,000 a month for a 2 bedroom apartment. Seriously.

The DOF has interpreted 581 as essentially requiring the use of rent regulated buildings for older co-ops and condos, however the Court of Appeals has indicated otherwise in TENNY v City of New York 2024 (discussed further below).

Nothing in the plain text of RPTL 581 requires municipalities to assess a luxury condominium or cooperative as if it were a regulated apartment where the properties differ in meaningful ways. Instead, the RPTL requires municipalities to treat condominiums and cooperatives like other similarly situated rentals. Therefore, to the extent that condominium and cooperative properties would not be subject to rent stabilization if they were not held in ownership, the proper comparable is a non-rent-regulated unit.

It is not clear how comprehensive the RPIE filings are for Market Rate rentals, however they are generally required for larger buildings so they are likely available.

Gross Income Multiplier - DOF estimates the gross income per square foot of comparable rentals and multiplies it by a factor to estimate market value. This is essentially the income capitalization method by another name. The key distinction is small buildings don’t have to file RPIEs so it’s a little more hand-wavey.

Replacement Cost - Technically the Reproduction Cost New Less Depreciation method. This is an estimate of the cost to rebuild the property. It is used for Class 3 (Utilities) and is calculated either by the NYS Office of Real Property Tax Services (ORPTS) or the NYC DOF depending on the type.

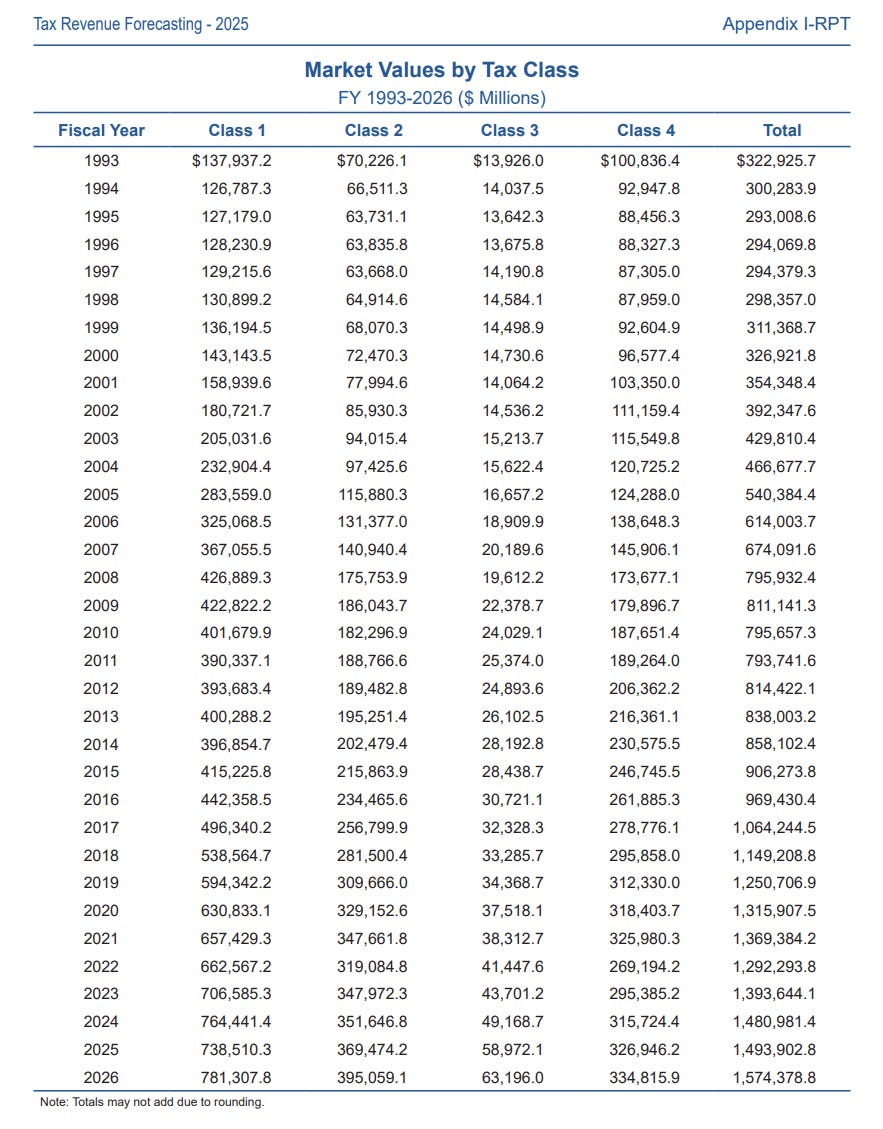

Here is how it all adds up

You might be wondering if every Coop, Condo and Rental in the city combined is really only worth $395bln. Probably not, but it underscores just how much using rent-stabilized comps for co-ops and condos lowers their valuation.

Assessment Ratio

After estimating a Market Value, the DOF applies an Assessment Ratio that State law requires is uniform for a given class. The Assessment Ratios are set administratively by the DOF pursuant to their powers under Section 1505 of the NYC Charter. Huh?

Yup, the DOF can simply change the class Assessment Ratios to anything between 0% 100%. This matters, but slightly less than you might think due to Assessment Caps Class tax share constraints detailed below.

The DOF has in fact done this several times since the passage of S.7000-A in 1981, the foundation of the current property tax system in NY. Class 1 began at 18% in 1983, was lowered to 8% in 1991, and finally to 6% in 2006 where it stands today. Class 2 and 4 began at 60% and were lowered to 45% in 1985. (sources disagree slightly on the exact years, perhaps due to calendar year vs fiscal year confusion. I went with the timeline from this 2006 IBO report)

Assessment Caps and Phase-Ins

Unlike the Assessment Ratio, these are not at the discretion of the DOF. The caps, which apply to Class 1 and Class 2a/b/c properties, set maximum annual and quinquennial increases in Billable Assessment Values. 6% per year and 20% every 5 years for Class 1 and 8%/30% for Class 2a/b/c. These caps are lifted when properties undergo substantial renovations, typically upon their completion and work sign-off by the DOB.

Classes 2, 3 and 4 have no Assessment Caps. Class 2 and 4 have 5 year phase-ins for Billable Assessment Value increases, but there is no hard limit, while Class 3 has no phase-in at all.

Take a Class 1 property that has a Market Value of $500,000 and a Billable Assessment Value of $30,000. Its Billable AV could increase by no more than 6% * $30,000 = $1,800 in the following year, even if the MV doubled to $1,000,000.

What happens to the caps if the DOF lowers the Assessment Ratio for Class 1? The cap, in terms of the actual tax bill, is effectively reduced or eliminated for that year. The extra piece that makes this work is the City is required to raise Class level Tax Rates to offset the lowering of Assessment Rates for reasons detailed later on.

Despite the 20% cap on 5 year assessment increases, somehow its tax bill quadrupled over the same period. Fun!

But don’t just take my word for it. The NYC Comptroller examined this in 2024 and concluded the same.

To emphasize, this is not a secret or me being especially clever. It is a key part of how the system works.

Exemptions and Abatements

These are largely governed by State law and are analogous to tax deductions (exemptions) and tax credits (abatements).

Exemptions reduce the Billable Assessment Value. Examples include the 100% exemption for Public Authorities like NYCHA, the 50% reduction for low income seniors and the controversial, now-expired 421-a program. The post-exemption value is referred to as the Taxable Value.

Abatements reduce the tax owed after multiplying the Taxable Value by the Property Class Tax Rate. Examples include the Co-op/Condo Abatement and the J-51 program (which has both an Abatement and Exemption component to make things even more confusing)

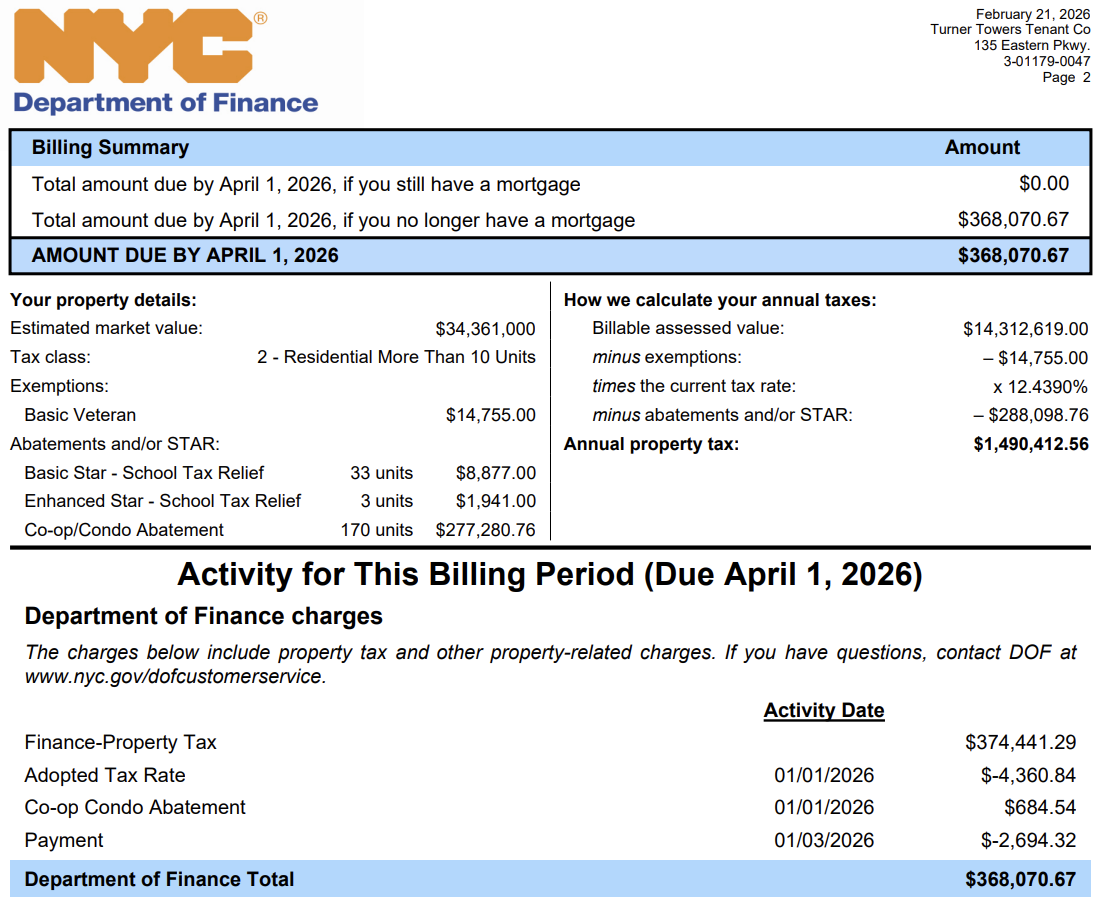

You can find these all on the quarterly property tax bills issued by the DOF:

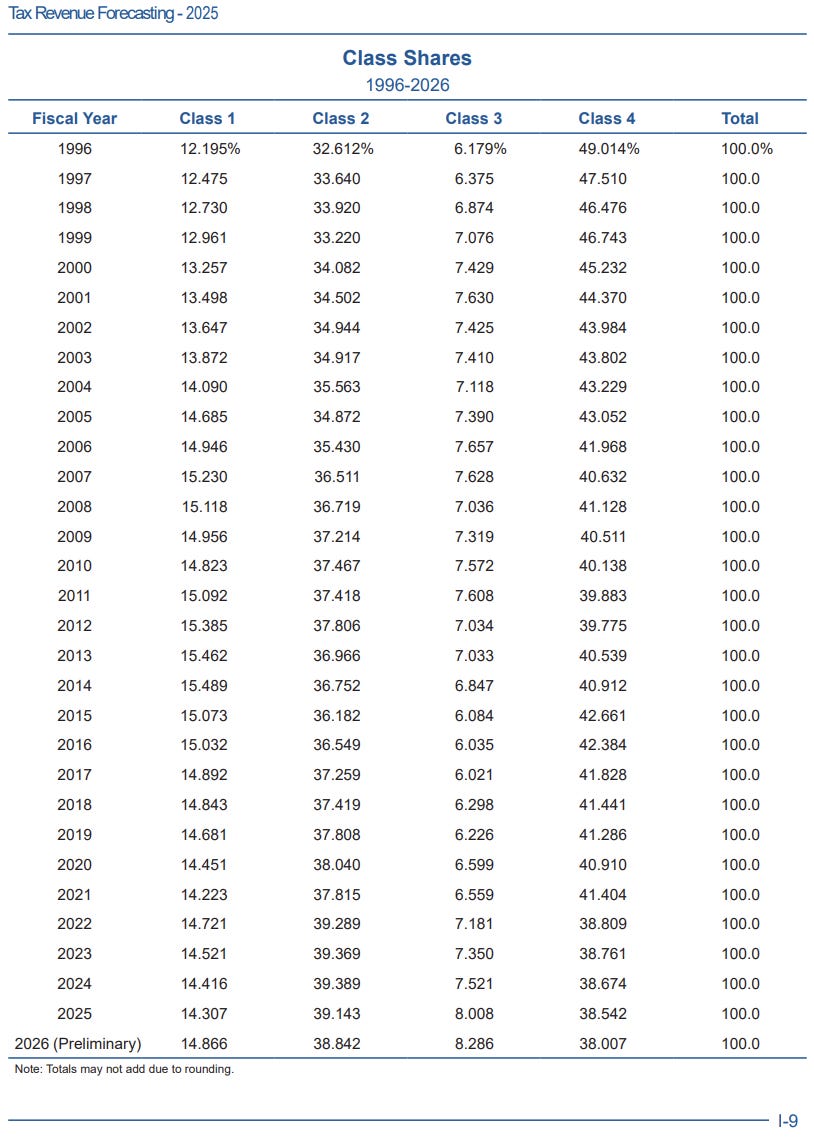

Class Share Caps

Another creature of State law, Class Share Caps limit how much the tax share of any one Property Class can change year to year. The maximum is 5% and State legislation can lower that to below 5% for NYC, as it has many many many times.

The 5% is relative to a Class’s current share of the overall levies, which are calculated after Exemptions are applied but before Abatements.

The Mayor’s Office of Management and Budget estimated that as 14.866% for Class 1 in 2026. That means its share can’t increase to more than 14.866% * 1.05 = 15.609% for 2027. This strictly limits how much the City can shift taxes between Property Classes in any one year.

Tax Rate

The Tax Rates are set annually at the Property Class level by the City Council, but their discretion is extremely limited. Due to DOF’s power over Assessments and the State limits on changes in Class Shares, the setting of tax rates is mostly formulaic.

The Council simply sets the rates at levels that preserve the relative Class Shares and, when multiplied by the Taxable Assessment Values, produces enough revenue to fund the Budget after accounting for non property tax revenues. If the budget is under-funded by other revenue sources, it is accounted for by an across the board increase in Tax Rates.

Assessment Reductions

There is also a process for property owners to appeal to the DOF to reduce their Assessments, which I will not detail here but am listing for completeness.

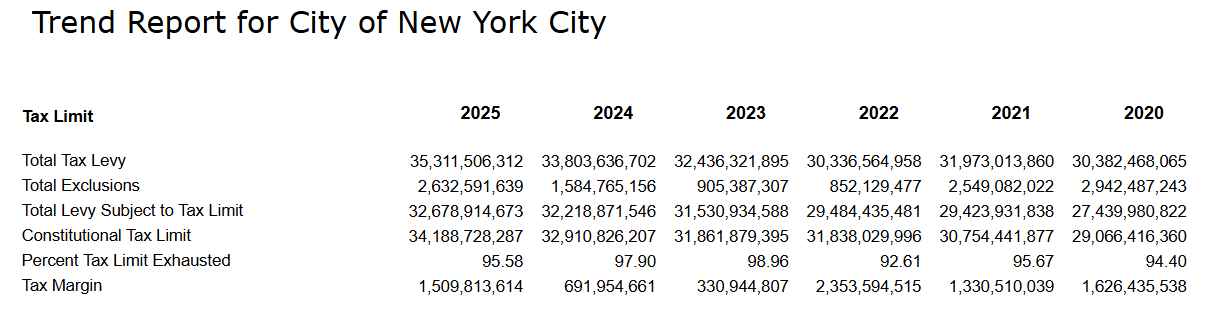

Constitutional Tax Limit

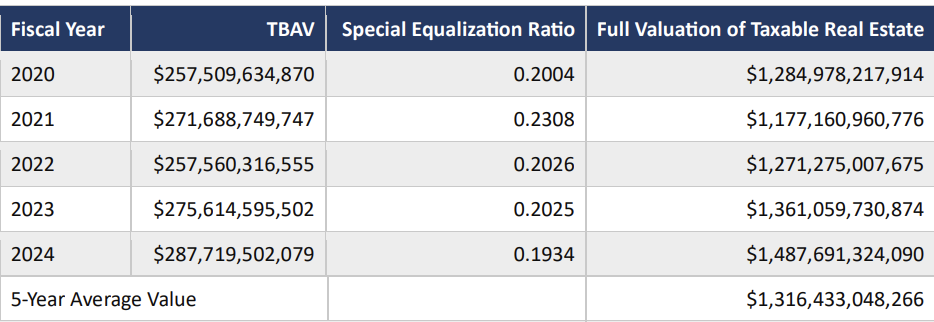

This is where it gets weird(er). Article VIII Section 10 of the NYS Constitution places a limit on the amount NYC can tax real estate. In substance, NYC cannot levy more than 2.5% of the five-year trailing average of the full valuation of taxable properties for Operating Expenses. The actual calculation of “full valuation” is slightly more complicated as detailed in the 2024 NYC Comptroller report, but it is practically as described above.

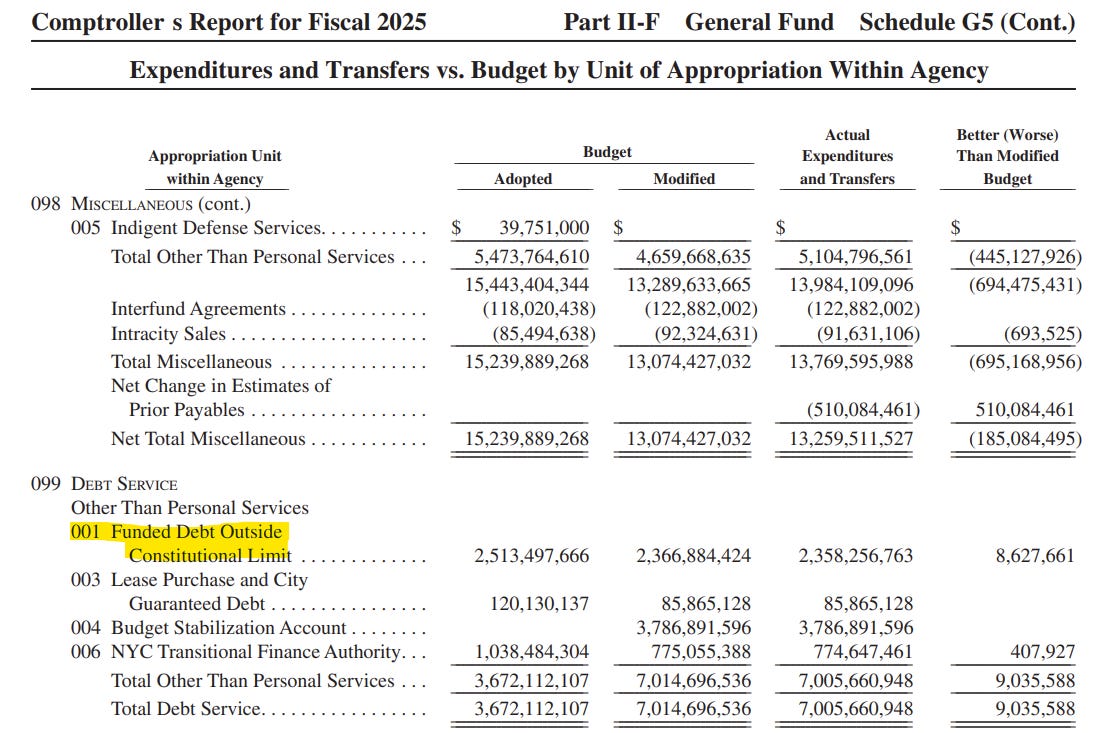

Property taxes for debt service on long-term bonds issued for capital purposes are not subject to the 2.5% limit. That’s likely the bulk of the 2.6bln number in the below State Comptroller report

The 2.6bln number is somewhat opaque as the detailed filings are not public. It appears to be the “Funded Debt Outside Constitutional Limit” in the Comptroller’s Annual Comprehensive Financial Report

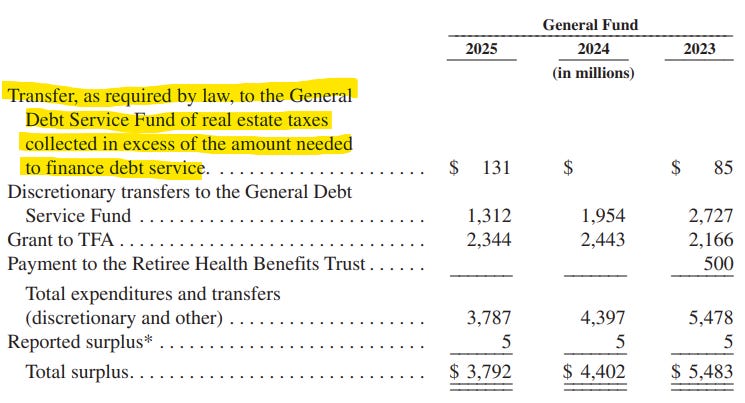

combined with the required transfers to the General Debt Service Fund for levies in excess of what was needed for that year

That still falls a little short of $2.6b of the exclusions in the State Comptroller report. The remaining difference may be from PAYGO financing exclusions authorized under Article VIII Section 11, which aren’t separately reported, or simply errors on my part. The general concept of the Constitutional Tax Limit [CTL] is straight-forward but its calculation is anything but.

A further wrinkle is that the “full valuation” essentially follows from the DOF’s practice of systematically undervaluing Condos and Co-ops as noted above. One scenario in the 2024 Comptroller report estimated the effect as $350bln for FY 2024. Though its focus was the debt limit (a separate 10% limit on indebtedness), the same “full valuation” is used for the 2.5% tax levy limit. That would have raised the cap by $8.75bln, providing plenty of room for increases.

Notably, NYC is quite close to this limit (95.58% in 2025) which may limit how much property tax rates may be raised. Nominally the debt service on NYC’s General Obligation bonds is a little over $4.4 billion for FY 2027, however that full amount can’t necessarily be excluded.

Large prepayments of future debt service in prior years limit how much of that $4.4 billion will actually be paid out of that year’s revenues. These prepayments have been steadily decilining though and current projections put them at just $238 million across all bond types.

That may leave just enough room for a potential 9.5% / $3.7bln increase in Property Taxes while maintaining a minimal buffer.

When the CTL is exceeded, the State Comptroller is required to withhold State Aid payments by the amount of the excess.

Yikes!

Limits on intra-class Inequity

Two parts of the State RPTL have increasingly come into conflict: the Class 1 Assessment Caps under RPTL 1805 and the uniform assessment requirement of RPTL 305. If some properties appreciate much faster than the Assessment Caps they will necessarily be taxed at a lower rate than slower appreciating properties.

Some decades ago, Coleman v County of Nassau tested this apparent conflict, albeit in a roundabout way we’ll gloss over. As summarized by a later decision, a class of property owners

contended that because market values for houses in affluent areas had increased sharply while market values had remained stagnant or declined in low-income areas, poor and minority homeowners were shouldering a disproportionate and discriminatory share of the countywide property tax burden

The County ultimately settled and, in a State-Court-approved consent decree, agreed to

“update and modernize [its] assessment rolls for residential properties,” and to “adopt a revaluation system and tax assessment roll to that end that [was] fair, nondiscriminatory, scientific and equitable”

To comply with the consent decree

the County’s only option was to lower the fractional assessment percentage for class one property

Nassau did exactly that and some property owners who lost their caps sued. The County’s lowering of Assessment Ratios was ultimately upheld in a 2007 Court of Appeals decision, O’Shea v Board of Assessors that weighs heavily on current litigation between Tax Equity Now New York LLC (TENNY) and the City of New York.

That case began in 2017, against both the City and the State, and is still proceeding in New York County Supreme Court, after a detour to the Court of Appeals. Building on O’Shea, the Court of Appeals in a 4-3 decision allowed the TENNY case to proceed against the City while allowing the State to be dismissed. The procedural details are complicated, but ultimately they are seeking for the City to reduce intra-class inequality within Class 1 (as in Nassau) and Class 2, which is somewhat novel.

TENNY is currently seeking summary judgement that the City is violating RPTL 305(2) as applied to Class 1 and Class 2 properties. Oral Arguments were held in October 2025 and a decision is pending

Reading the tea leaves a little, it seems unlikely the Judge will immediately require the City to lower Class 1 Assessment Ratios and change the Class 2 valuation methodology for co-ops and condos. However, that is ultimately the direction this appears to be headed, in my opinion. Whether it gets there via several more years of litigation, voluntary changes by the City, or State level reforms remains to be seen.

Who wants to create a Polymarket for this?