NYC Undertaxes Its Most Expensive Homes. One Simple Change Could Fix It

The City doesn't need Albany to fix Class 1 property taxes. It just needs to act. Part 2 of an assessment of NYC property taxes

Following an overview of how property taxes are calculated in NYC, this post looks at the effects of those calculations on Class 1 properties, i.e. 1-3 family residential homes.

It will also discuss how the NYC Department of Finance, without the need for any City or State legislation, can end the disparities discussed herein.

Recap of Class 1 Tax Calculation

Each year, through DOF assessments and the City budget process, taxes are set on properties in NYC.The abbreviated process is:

DOF estimates the market value of every 1-3 family home based on comparable sales. These estimates, while not perfect, are pretty good!

DOF then multiplies the market value by their assessment ratio, currently 6%, to get a tentative assessed value

That assessed value is then capped at a maximum increase of 6% per year and 20% per five years

Then any exemptions, like low-income senior programs, are subtracted from the capped assessment value

Finally, the capped and exempted assessment value is multiplied by the tax rate and abatements are subtracted from the final bill. For FY26 the tax rate is 19.843%

[cap(Market Value x Assessment Ratio) - Exemptions] x [Tax Rate] - Abatements

One additional wrinkle is that the tax share per class can’t increase by more than 5% in any given year, so the tax rate is set at a level that keeps the proportion of taxes paid by class fairly constant.

How This Maps Out

The most critical feature of the Class 1 tax calculation is the assessment cap. Market values are what they are and don’t get capped, but the assessed value that tax rate is applied to can’t increase by more than 6% a year.

Areas with high growth see their assessments rise at a much lower rate as a result. The side effect is that every other Class 1 property has to pay higher taxes to offset those caps, since the total amount of taxes paid by Class 1 has to stay proportionate year over year.

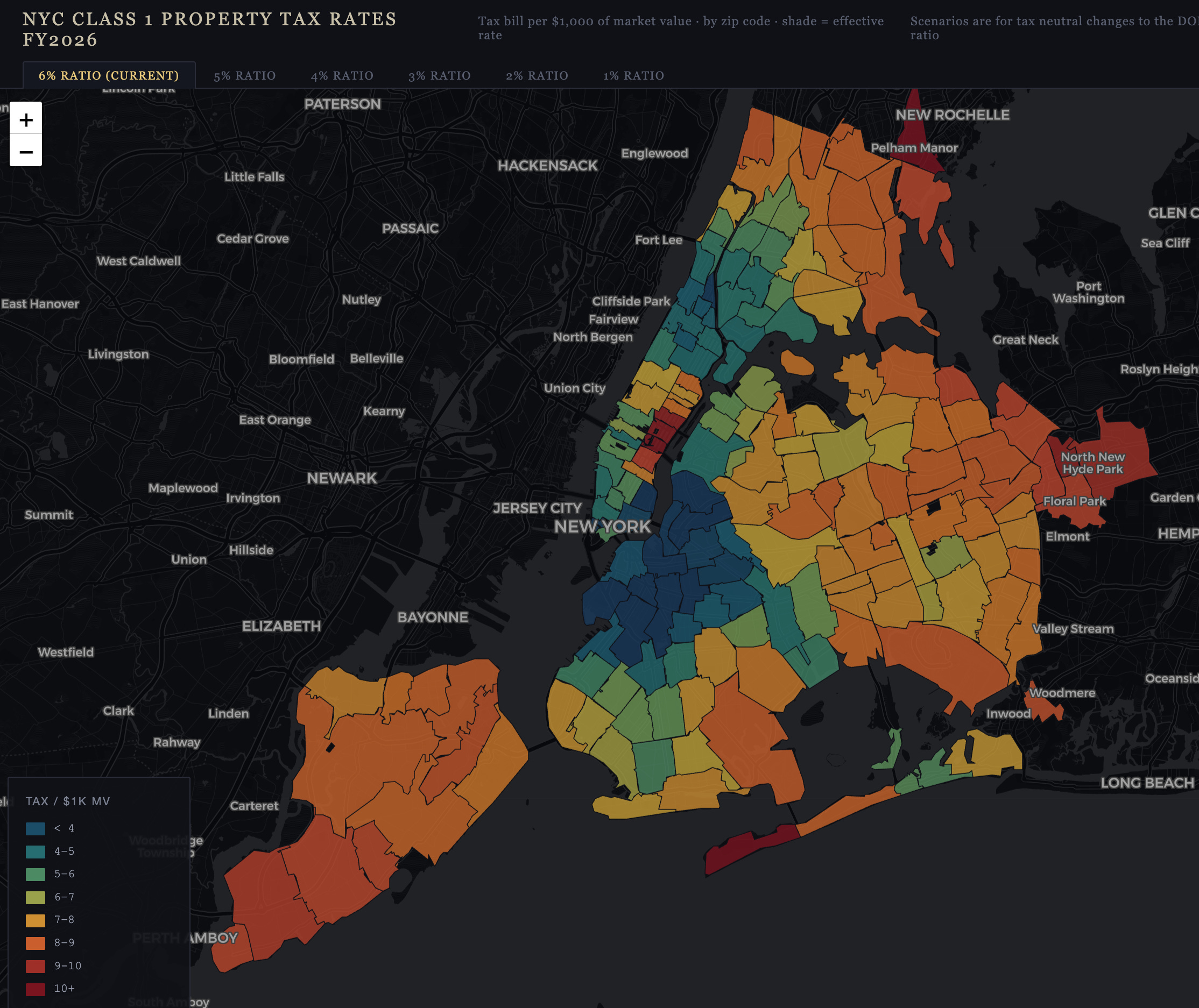

This is exactly what we see when we take the tax bill each 1-3 family homeowner pays and divide it by the DOF market value. The average homeowner in Brownstone Brooklyn is paying about 0.3%, or a mill rate of 3 in property tax jargon. Meanwhile, folks in the slower growth neighborhoods of Eastern Queens, Staten Island, and the Bronx are paying $8, $9, or $10 per $1,000 of market value.

This is not good!

No one argues that rowhouses in St. George should pay 3x the rate of brownstones in Park Slope and yet that’s the result we have.

How to Fix It

Mechanically, this is easy. The City’s Department of Finance can simply lower the assessment ratio. Yes, really. No City or State legislation required. It probably doesn’t even need to go through the formal rulemaking process (CAPA).

Lowering the assessment ratio effectively raises or removes the assessment cap in a given year. Here’s a simple illustration of how that works for a single property.

The billable assessment value never goes up by more than 6% per year, but the tax bill quadruples over five years. The Comptroller also published a great report on this effect in 2024.

This works because the State law that caps Class 1 assessments applies only to the assessments. Lowering the assessment ratio while raising the tax rate is entirely permitted, as long as the tax rate stays below 100%.

The practical limit of how low assessment ratios can go is just under 1% due to that 100% cap on tax rates. But that’s plenty to work with!

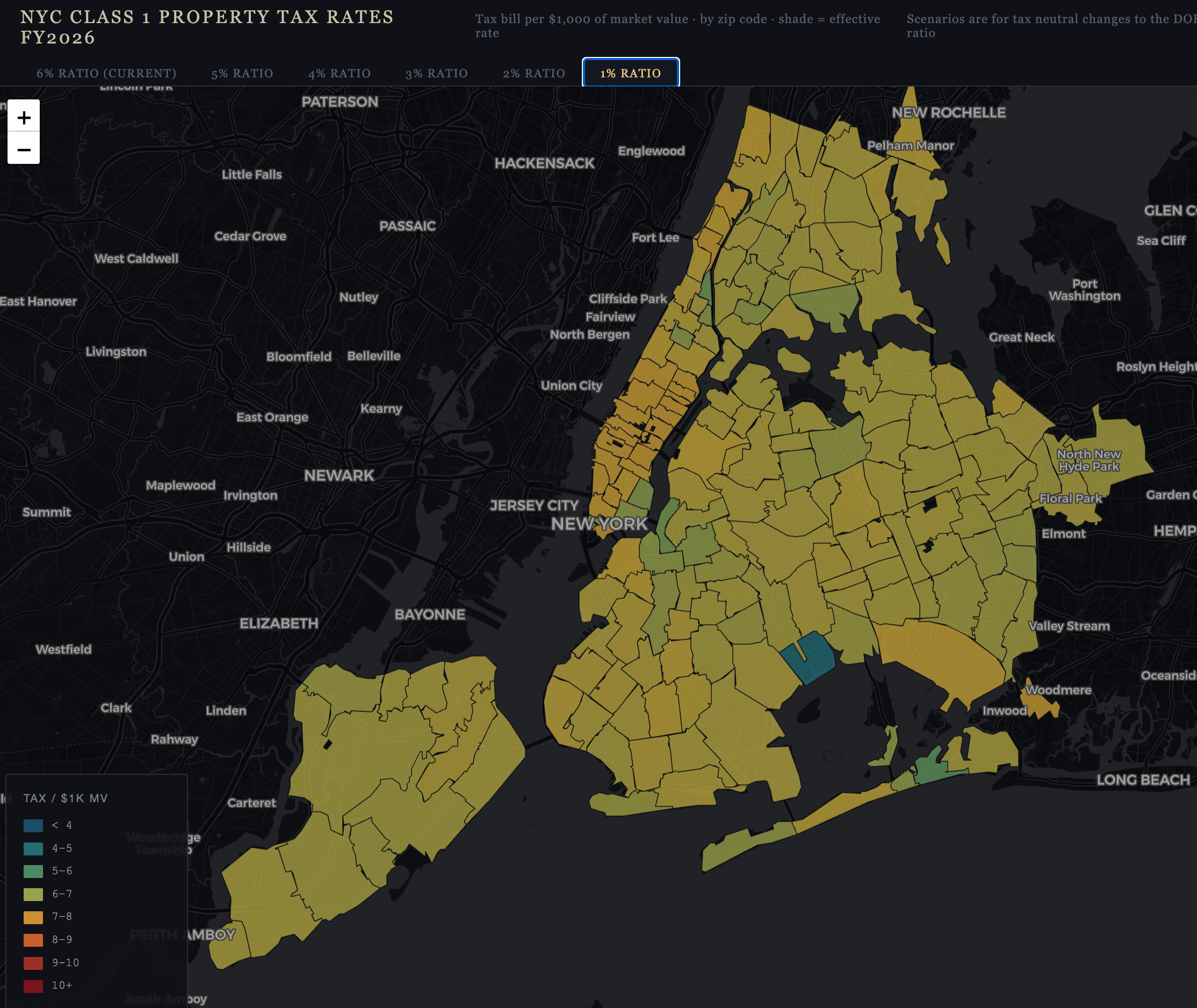

Here’s what effective tax rates would look like if we lowered the ratio to 1% and raised nominal rates to 72%, keeping total Class 1 tax revenue neutral.

Although this map isn’t as aesthetically pleasing as the above one, it is much much more equitable. Click through the tabs in the map to also see the effects of lowering the ratio by different amounts and hover over the shaded zip codes to see more details.

Why Doesn’t The City Just Do This?

There are some arguments against making a change like this, some may be more persuasive than others. The ones I’m aware of are:

Removing the assessment caps will mean some property owners’ tax bills quadruple overnight!

This is basically true and can be destabilizing for house-rich, cash-poor folks who’ve lived in their homes for decades, but it can be softened by phasing in the assessment ratio reductions. Going to 5% this year, 4% next year, and gradually easing in over the next decade is entirely possible. And besides, the 0.12% tax on this $12 million landmarked limestone along Prospect Park probably should be quadrupled.

This is only a temporary fix and doesn’t solve the underlying problems in the tax code

Yes, this only raises or removes the cap in the year the ratio is changed, but that buys us potentially decades before the inequality gets this bad again. Marginal improvements are still improvements!

Property tax reform is a third rail, it would cost a lot of political capital to do this

These changes would benefit a lot of people somewhat and cost some people a lot. Further, the losers skew progressive democrat while the winners skew conservative. Those are simply tough politics to work with for a progressive mayor, who’d ultimately be responsible for directing the DOF to make this change

The City May Have To Even If They Don’t Want To

There is a long-running lawsuit between Tax Equity Now NY (TENNY) and the City of New York that, among other things, seeks to compel the city to lower Class 1 assessment ratios.

Nassau County was pushed into a settlement doing exactly that, following similar litigation, and is heavily cited by the plaintiffs.

A decision is forthcoming on TENNY’s claims aimed at fixing Class 1 and Class 2 property inequities. My own guess is that those claims survive the City’s motion to dismiss and they proceed to discovery. But summary judgement either in favor of TENNY or the City seems very unlikely after nine years of litigation.

All said, even if the City declines to use its powers to reform property taxes, we may see the courts force it to act within the next few years.

Mildly interesting. I’m in favor of marginal improvements and equity in tax burden. Interesting point about the political skews of beneficiaries and those “harmed.” The table was a little hard to read at first, btw.

Mildly interesting. I’m in favor of marginal improvements and equity in tax burden. Interesting point about the political skews of beneficiaries and those “harmed.” The table was a little hard to read at first, btw.