Update on the Constitutional Tax Limit

It is very unlikely you want to read this, but if you just can't get enough of the CTL and want to see what the actual filings look like, proceed!

I made an attempt at explaining the limit on property tax levies imposed by the NYS Constitution. It left some open questions on exactly what exclusions the City uses in its calculation of the limit and just how close the proposed FY27 budget gets.

NYC and NYS Comptroller’s Supporting Documentation

Less than two weeks later, we have answers! The City Comptroller’s comment on the budget has a section dedicated to the calculation (scroll down to “The City’s Operating Limit”) and the State Comptroller provided the last 10 years of the City’s official filings. Thank you, Mark Levine and Thomas DiNapoli!

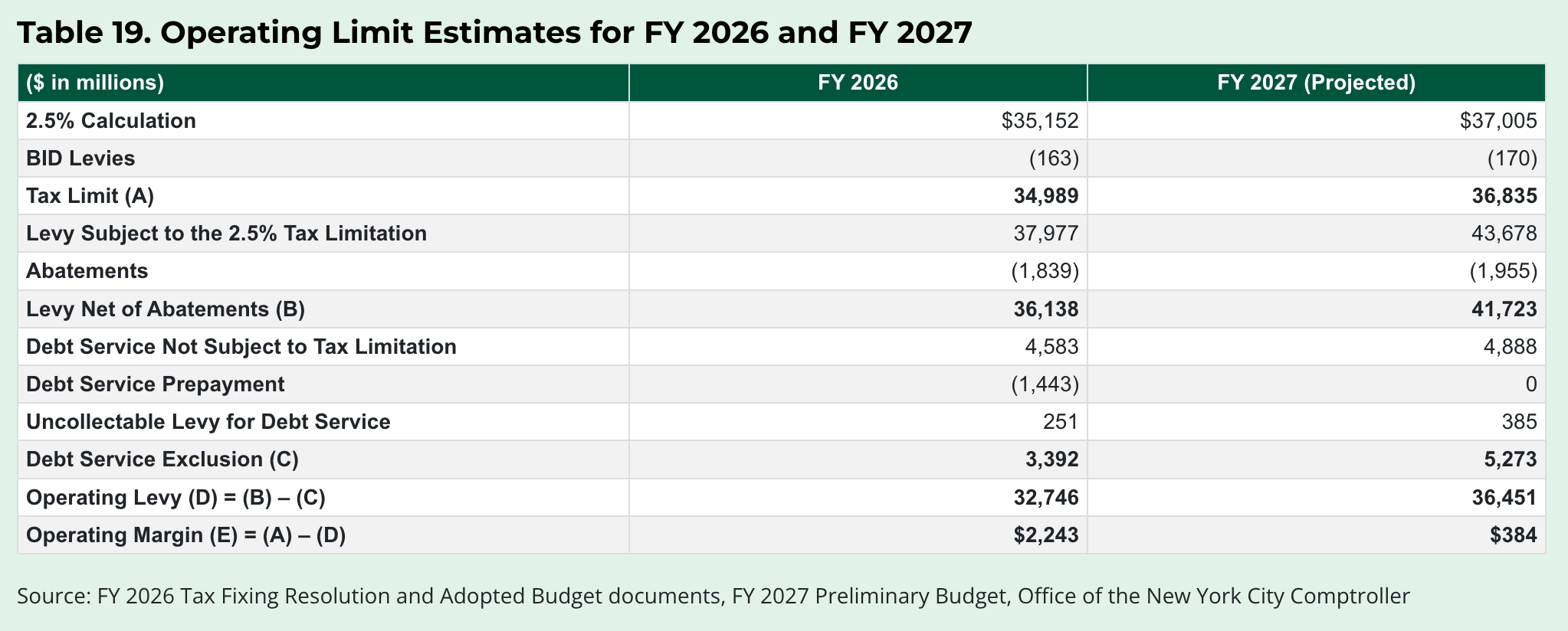

There you have it. The Comptroller estimates $384 million of room to spare in FY27 after excluding $1,955 million of abatements, $4,888 million of debt service and $385 million of uncollectable taxes. This is inclusive of the proposed 9.5% increase in property tax rates.

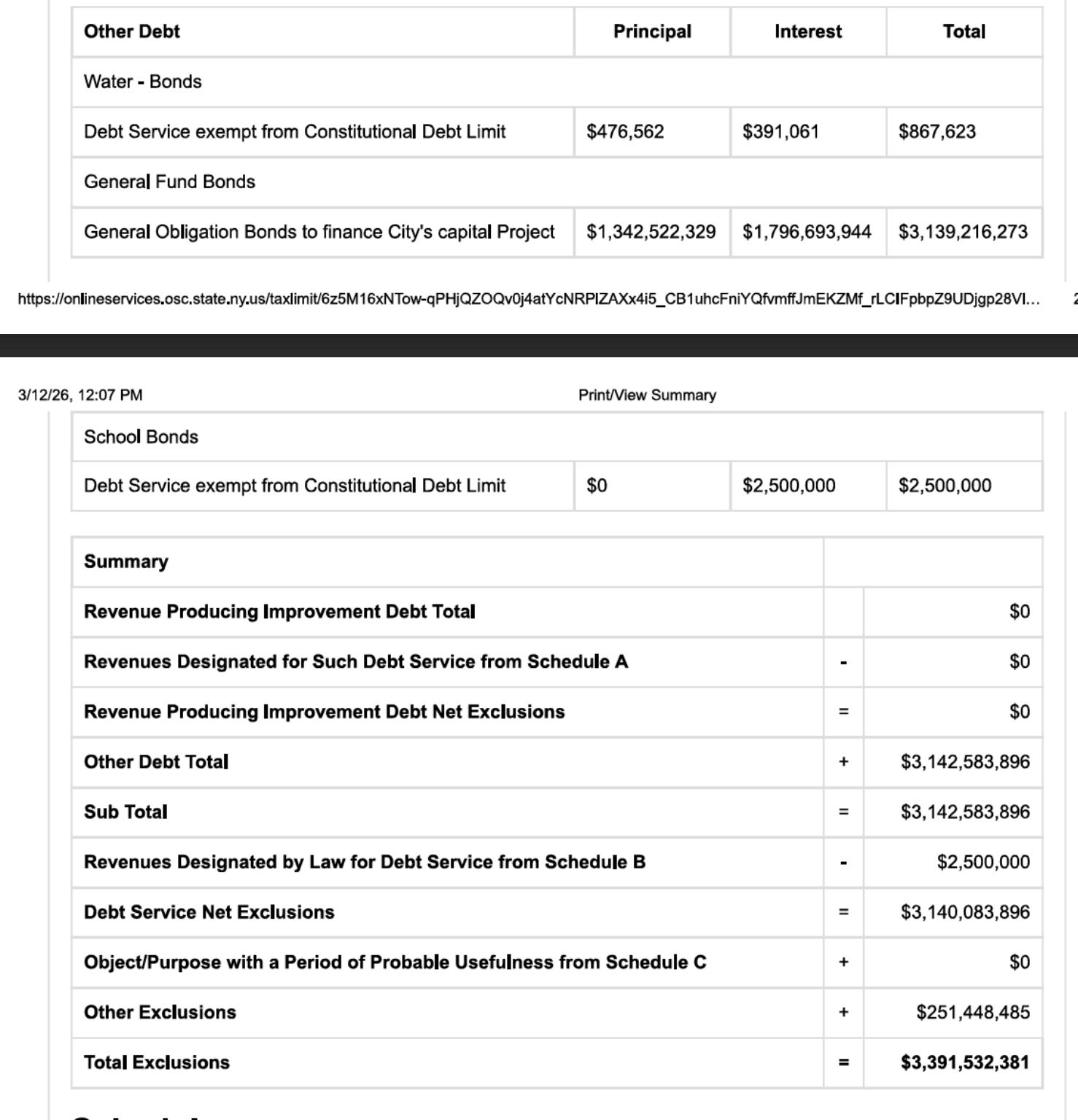

The debt service exlcusion, judging from the prior year filings, is virtually entirely from GO bonds. The Other Exclusions in the filing correspond to the Uncollectable Levy for Debt Service. Everything squares more or less.

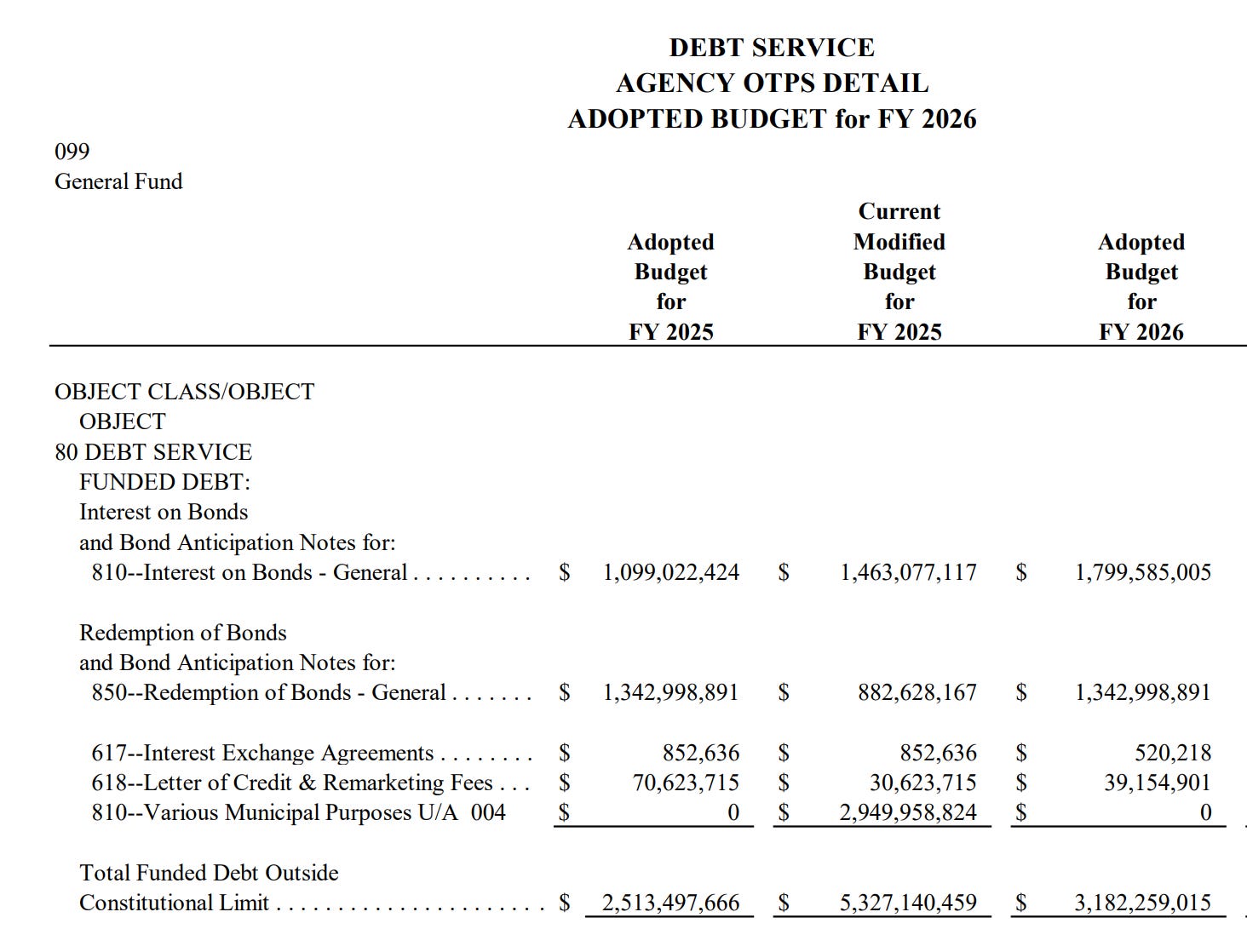

The “less” part is a $40 million downward adjustment “to account for NYS building aid and other components” from the $3,182 million you’d see in the Expense, Revenue, Contract Budget adopted in June 2025 (warning: 800+ pg PDF).

Takeaways

There are a few things that fall out from the mechanics of this calculation

The City can raise property tax rates by 9.5% and stay within the CTL, albeit barely

The CTL filing is made shortly after the budget is adopted. The FY26 filing was made in July of 2025.

The GO bond debt service, minus prepayments from prior years, is fully excluded.

The prepayment for the subsequent fiscal year is not excluded because it’s not in the adopted budget. It ends up there in the modified budget approved in the following year.

Because expected prepayments of GO debt to the BSA are not in the filings, the actual usage of the limit often realizes lower than what’s in the filings.

There are no expected prepayments from FY26 to FY27, so debt service exclusions for FY27 are particularly high, supporting a higher effective property tax limit.

The uncollectable tax projections are very high for FY27, up $130 million from FY26 and doubled from FY25. There may be a story about property tax collection rates and the suspension of tax lien debt sales?

NYC Constitutional Tax Limit Filings for FY2017 through FY2026

These were obtained via a FOIL request to the NYS Office of the Comptroller. These are the actual filings the City made, typically 1-2 months after the adoption of the budget, to demonstrate compliance with the 2.5% limit on the property tax levy. Enjoy!